Tech Gaps Down Into PCE Week. SPY 745, QQQ 738, Gold 4,146. Tuesday’s Map.

The Iran deal is signed, oil is at three-month lows, and the war premium is gone, but the tape woke up red anyway. SPY is indicated down 1.27 percent and QQQ down 2.60 percent premarket, with Alphabet

Roy’s Market Insights | SPY, QQQ and GOLD Premarket Roadmap | Tuesday, June 23, 2026

For months, the bull case had a simple villain. The war in the Middle East was the thing pinning the tape down, the reason oil kept spiking and inflation kept running hot and the Fed kept its foot on the brake. Remove the war, the thinking went, and the market clears its throat and runs. Well, the war is over. The memorandum of understanding got signed at Versailles last Wednesday, Hormuz is reopening, and crude has fallen off a cliff. So this morning we get to find out what the market actually does when it gets exactly what it asked for.

The answer, so far, is sell.

Start with the relief itself, because on paper it is everything the bulls wanted. The US-Iran deal is signed, the Treasury has granted Iran a 60-day license to sell oil, and WTI has collapsed to roughly 74 dollars with Brent near 77.50, both at their lowest since early March. The geopolitical risk premium that hung over equities since February is simply gone. And yet Monday closed lower, with the S&P 500 off 0.37 percent and the Nasdaq Composite down 1.32 percent, dragged by a 5 percent slide in Alphabet on AI talent-departure concerns, a 4.8 percent drop in Amazon, and a 3 percent fall in Microsoft. The premium left the tape, and the tape kept falling.

When the risk that was supposed to be holding a market down disappears and price still rolls over, the message is that the problem was never the thing you were watching. The problem here is the Fed. Kevin Warsh’s first meeting on June 17 delivered a hawkish shock dressed up as a hold. Rates stayed at 3.50 to 3.75 percent on a unanimous 12-0 vote, but the dot plot flipped from an implied cut to a hike-leaning median of 3.8 percent, with nine of eighteen participants now penciling at least one hike this year and seventeen of eighteen judging inflation risks to the upside. The dollar index ripped to a 13-month high. The 10-year sits near 4.46 percent. Markets now treat a September hike as the live scenario, and both Deutsche Bank and BofA have moved their base case to a cut-free path. The oil relief that should have eased the inflation math is being buried under a new chair who told you, in the plainest language he could use, that this committee intends to deliver price stability and is done with forward guidance.

That collision, fading geopolitical risk against a hardening rates picture, is what the premarket is pricing this morning, and it is not pretty. SPY is indicated at 734.90, down 1.27 percent against Monday’s 744.39 close. QQQ is indicated at 718.74, down 2.60 percent against its 737.95 close, the sharper move because the selling is concentrated exactly where it always is, the mega-cap AI complex. This is a gap-down open, not a drift. Gaps like this, dropped into a quiet-data Tuesday that sits two sleeps in front of the week’s only real catalyst, tend to do one of two things: snap back hard as the overnight panic gets faded, or confirm the breakdown and trend lower all session. There is rarely a calm, balanced middle. The first hour usually tells you which one you are living in.

The calendar fills in the rest. Today is light, flash PMIs plus Carnival and FedEx earnings, with FedEx the more useful tell as a read on whether the Hormuz reopening is starting to show up in global shipping economics. Wednesday brings Micron, the single most important earnings event of the week and a direct referendum on the AI memory trade that has carried this index. Then Thursday, June 25, at 8:30 AM EST, the week resolves on May PCE, the Fed’s preferred inflation gauge, landing right on top of Warsh’s freshly raised forecasts. Consensus has headline PCE climbing to roughly 4.1 percent year-over-year and core near 3.4 percent, hotter than CPI, with final Q1 GDP and jobless claims stacked alongside it. A hot print validates every dot on that plot and hands the September-hike camp the data it wants.

So the read for today is clean enough to say in a sentence. The structure says distribution, the calendar says the real test is Thursday, and the open is really just one question asked over and over until it answers itself: does the gap hold, or does it fill.

The Institutional Snapshot

SPY · QQQ · Gold | Tuesday, June 23, 2026

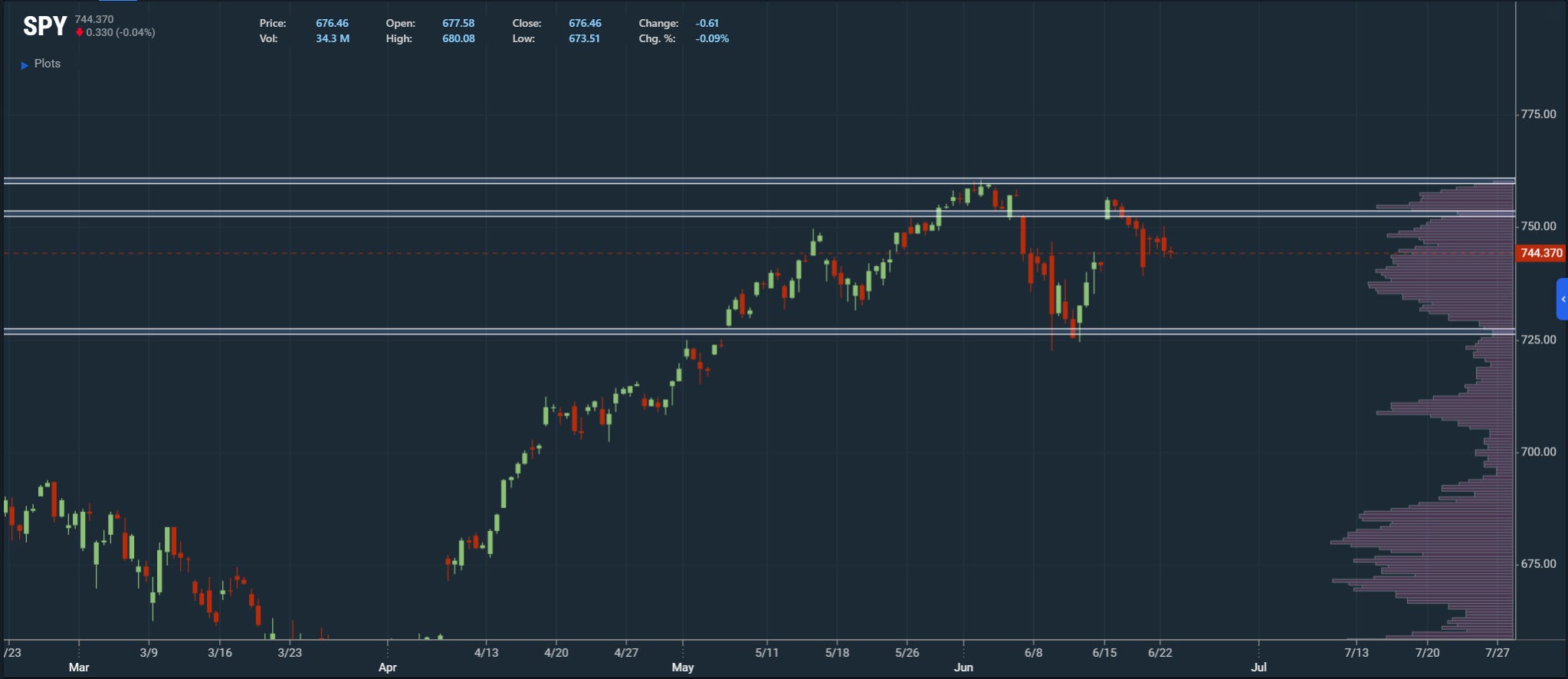

SPY Monday close: $744.39 (-2.35, -0.31%), intraday range $743.13 to $750.18

SPY premarket: $734.90 (-9.49, -1.27% vs prior close)

QQQ Monday close: $737.95 (-1.86, -0.25%), intraday range $734.39 to $745.45

QQQ premarket: $718.74 (-19.21, -2.60% vs prior close)

Gold: front-month futures ~$4,146, spot ~$4,150 to $4,166, heavy near the long-term floor under a 13-month-high dollar

WTI crude: ~$74, lowest since early March on the Iran deal and the Hormuz reopening

Brent: ~$77.50, near three-month lows

10-year yield: ~4.46% after the hawkish FOMC

Dollar index: 13-month high, the dominant pressure on gold

VIX: ~17.3, low despite the gap, the panic is concentrated, not broad

Macro arc: US-Iran MOU signed June 17, Hormuz reopening, oil at three-month lows; Warsh’s June 17 FOMC held but flipped the dot plot hawkish, dollar at multi-month highs

AI unwind: Monday’s leg led by Alphabet -5% (AI talent concerns), Amazon -4.8%, Microsoft -3%; QQQ premarket -2.60% extends it

8:30 AM EST Thursday June 25: May PCE is the dominant catalyst (consensus headline ~4.1% YoY, core ~3.4% YoY), with final Q1 GDP and jobless claims alongside

September Fed hike odds: now the live scenario; 9 of 18 dots see a 2026 hike, median 3.8%, 17 of 18 see upside inflation risk

Earnings this week: FedEx and Carnival today, Micron Wednesday, the AI referendum

Next major catalyst: PCE Thursday; Micron Wednesday is the earnings wildcard

The Setup: The War Premium Left, and the Tape Still Fell

The bulls have a clean story they cannot get the tape to honor. The war is over, oil has collapsed, the geopolitical risk premium that hung over equities since February is gone, and the VIX is sitting under 18. On paper, that is the all-clear. If the AI selling is a one-name Alphabet story rather than a complex-wide unwind, the gap-down open is a gift, and the snap-back fills it by lunch.

The bears have the only thing that has mattered since June 17: the Fed. A market that sells off as its biggest tail risk resolves is a market telling you the resolution was already priced and the next move is about rates. The dollar at a 13-month high, the 10-year near 4.46 percent, and a dot plot that flipped to a hike are not a backdrop that rewards owning long-duration mega-cap tech. The Alphabet-led leg is the symptom; the disease is a discount rate that just got marked higher with PCE two days out to confirm it.

What the tape needs to decide today is whether this gap-down is an overnight overreaction to be faded or the start of a distribution leg into the print. There is no data today big enough to override the gravity of Thursday’s PCE, so the cleanest read is that the open is a referendum on the gap itself: hold it and the breakdown extends, fill it and the bounce buys time. Three scenarios stay in play.

In the snap-back path, the gap gets faded on the open, the Alphabet story stays contained to one name, and price reclaims the prior-day levels as the overnight panic drains. In the distribution path, the gap holds, sellers use any bounce to distribute, and price grinds lower toward the next shelf as the AI complex stays heavy into Micron and PCE. In the balance path, price stabilizes below the prior close but above the deeper supports, chopping in a wide gap-down range as nobody commits size ahead of Thursday.

Higher Timeframe Structure — SPY

SPY closed Monday at 744.39 after a two-week stretch that ran from the early-June highs at the 760 zone, through the post-FOMC fade, and into a lower range that has been carving out between roughly 744 and 752. The index spent last week rejecting the 750 to 752 supply and is now gapping down through its own base. The 760 area still marks the failed 52-week high above. The 725 zone marks the deeper shelf that held the early-June flush below.

The HTF read: with premarket at 734.90, SPY is gapping below the entire recent base and pointing at the 731 to 732 volume shelf that has acted as the lower edge of the post-selloff range. Above, 744 to 745 is now resistance rather than support, the level the index has to reclaim to neutralize the gap, then the 750 to 752 supply, then the 760 highs. Below, 731 to 732 is the first real floor, then the heavier 725 shelf that defined the June flush low. As long as SPY holds above 725 on a closing basis, the larger structure is a wide post-FOMC range, not a breakdown. Lose 725 with acceptance and the picture turns into a deeper retracement of the spring advance toward the 718 to 720 zone.

Higher Timeframe Structure — QQQ

QQQ closed Monday at 737.95 and is the epicenter of this move, because the leadership getting sold, Alphabet, Amazon, Microsoft, and the broader AI mega-cap complex, is exactly what this index is built on. After tagging the 748 highs in early June and chopping in a 725 to 745 range through the FOMC, the premarket at 718.74 has it gapping clean below the entire recent structure and pointing at the deeper supports.

The HTF read: this is the most macro-sensitive and most concentrated index on the board, and the gap proves it, down 2.60 percent against SPY’s 1.27 percent. Above, the lost 725 base is now the level to reclaim, then 732 to 733, then the 745 to 748 highs. Below, the premarket is already pressing toward the 713 to 716 zone, then the critical 705 to 707 base that held Friday’s flush in the prior cycle, then the deeper 697 to 700 area. QQQ’s behavior today tells you whether the AI trade is undergoing a genuine repricing or just a violent one-name gap that fills. Micron Wednesday and PCE Thursday are the triggers that resolve it.

Higher Timeframe Structure — Gold

Gold front-month sits near 4,146 with spot around 4,150 to 4,166, having broken down hard from the 4,365 area it held in early June and now consolidating just above the major long-term floor near 4,040. The metal is caught in a brutal one-way setup: the hawkish Fed and a 13-month-high dollar are pressing it lower, and the one force that used to hold a floor underneath, geopolitical risk, has evaporated with the Iran deal. Safe-haven demand drained at exactly the moment the dollar took off.

The HTF read: gold has lost the 4,300 shelf that capped it for weeks and is now leaning on the 4,040 long-term monthly floor as the line that matters. Overhead, 4,300 is the first reclaim level, then the 4,400 zone, then the heavier 4,680 resistance shelf far above. Below, 4,040 is the structural floor that has held this entire correction from the January highs above 5,600. Gold’s macro tell is the cleanest on the board: it is not catching any bid at all, which says the rates and dollar story is completely in control and the geopolitical hedge has been unwound. That is the same hawkish backdrop pressing on long-duration tech, and it lines up with everything the bond market and the dollar are saying ahead of PCE.

🔒 The intermediate structure, intraday execution levels, and three scenario maps for SPY, QQQ, and Gold are below for paid subscribers.

SPY premarket 734.90, QQQ premarket 718.74, both gapping down hard into a tape that has every reason to stay heavy with the AI complex under pressure and May PCE two sleeps away on Thursday. The map below has every level, every scenario trigger, and the playbook for the gap-fill snap-back, the wide gap-down balance, and the distribution leg lower.