Records Set, Iran Breaks Off Talks, Oil Cools the Spike. Cracks Under the Glass. Tuesday's Map.

All three indexes closed at fresh highs. Iran suspended communications with Washington. Oil spiked 6% then pulled back this morning. JOLTS at 10 AM.

Roy’s Market Insights | SPY, QQQ and GOLD Premarket Roadmap | Tuesday, June 2, 2026

Yesterday looked like a celebration. The print underneath says otherwise.

The Dow closed above 51,000 for the first time in history. The S&P 500 finished its ninth straight winning week, the longest streak in over two years. The Nasdaq Composite added another 0.42%. SPY closed $758.54 after tagging a fresh ATH at $760.28. QQQ closed $742.74 up 1.82% after hitting $745.65 intraday. Three indexes, three records, capped by an ISM Manufacturing PMI print of 54.0, a four-year high and a hard fundamental anchor under the AI-infrastructure trade. NVDA ripped 6% on the new RTX Spark Superchip launch, its entry into the PC market. Dell jumped 10% on earnings. IBM and Salesforce each added more than 7%.

Then the tape did three things that don’t usually happen on a record-setting day.

VIX rose 4.77% to 16.05 at Monday’s close and is bid again this morning at 16.14. Volatility lifting into new highs is the textbook divergence signal. The Russell 2000 fell 0.38%. Energy was the only other sector in the green besides tech. Only 52% of S&P 500 stocks closed above their 50-day moving average. The headline was a record. The breadth was narrow.

After the close, the Iran story reversed completely.

Iranian state media reported Tehran had suspended communications with Washington following fresh strikes near Lebanon, with a renewed threat to fully close the Strait of Hormuz. The tentative 60-day MOU we were tracking Friday now sits in question. WTI surged 5.93% intraday Monday on the headline. The interesting tell this morning: WTI is back to $91.17, down 1.07% on the session. Brent $93.82, down 1.22%. The market is taking the Hormuz threat seriously enough to keep oil elevated above last week’s $87 lows, but not seriously enough to extend the spike. That nuance matters.

The bond market did extend. The 10-year yield climbed back to roughly 4.50%. The 2-year hit its highest level since February 2025. December rate-hike odds, hike not cut, now sit above 60%. Goldman Sachs warned crude could stay at $90 through year-end even if the strait reopens. The Atlanta Fed cut its Q2 GDPNow estimate to 3.0% from 3.8%.

This is the first real blow to the disinflation thesis that powered nine consecutive winning weeks.

The setup today: indexes at records, oil cooling the spike but still elevated, yields holding near the highs, VIX bid, geopolitics reversing, and JOLTS Job Openings at 10:00 AM EST as the morning’s first labor read into Friday’s NFP. The bull case has not broken. It has been tested for the first time in a month. The premarket is mildly red. SPY $757.09, QQQ $741.85. A flat-to-down open against this backdrop is the tape choosing to digest, not capitulate. That choice matters.

The Institutional Snapshot

SPY · QQQ · Gold | Tuesday, June 2, 2026

SPY Monday close: $758.54 (+$2.06, +0.27%), intraday range $754.69 to $760.28 (new 52-week high)

SPY premarket: $757.09 (-$1.45, -0.19%), pulling back from the record

QQQ Monday close: $742.74 (+$13.29, +1.82%), intraday range $735.99 to $745.65 (new 52-week high)

QQQ premarket: $741.85 (-$0.89, -0.12%), digesting yesterday’s rip

Gold futures: $4,563, holding the post-reversal compression

WTI crude: $91.17 (-1.07% this morning), pulling back after yesterday’s 5.93% intraday spike

Brent: $93.82 (-1.22% this morning)

10-year yield: ~4.50%, holding near the recent high

2-year yield: highest since February 2025

VIX: 16.14, bid again after closing +4.77% to 16.05 Monday, divergence at the highs

ISM Manufacturing PMI: 54.0 (4-year high, beat 53 forecast)

NVDA +6% on new RTX Spark Superchip launch (PC market entry); Dell +10%, IBM +7.34%, Salesforce +9.57%

Dow closed above 51,000 first time ever; S&P 500 ninth straight winning week

Iranian state media: Tehran suspended communications with Washington, renewed threat to fully close Hormuz

Goldman Sachs: crude could stay at $90 through year-end even if strait reopens

Atlanta Fed GDPNow Q2: cut to 3.0% from 3.8%

Fed December rate-hike odds: above 60%

10:00 AM EST: JOLTS Job Openings (April) — prior 6.9M

Russell 2000 -0.38% Monday; only 52% of S&P stocks above 50-day MA

Broadcom and CrowdStrike earnings this week; NFP Friday

The Setup: Records With Warning Lights

The tape has been one-way for nine weeks. Yesterday added a tenth potential leg with three simultaneous records and an ISM beat, and immediately picked up four pieces of evidence that the trade is getting crowded: VIX rising at the highs, narrow breadth, oil spiking, yields jumping. None of those individually breaks the bull case. All four together, on the same session, is the first time since April we have seen this pattern.

The mitigating tell this morning is the oil pullback. WTI giving back some of yesterday’s gain says the market is treating the Hormuz threat as elevated risk, not active crisis. That gives the tape some room to digest rather than gap down. But oil is still above $91 versus last week’s $87. The risk premium is now embedded.

Three scenarios stay in play for Tuesday.

The market shrugs off the Iran reescalation the way it has shrugged off every other Iran headline since April. JOLTS comes in line or soft. Yields stabilize. Oil keeps cooling. The record-day breadth concern is forgotten by the close. SPY presses back at $760, QQQ retests $745. That is the continuation path, and it is the path that has paid for nine weeks running.

The market digests. Indexes rotate between yesterday’s range and the breakout shelves below. JOLTS prints a wash. The Iran story stays in the background but doesn’t escalate further. SPY balances $755 to $760, QQQ rotates $738 to $745. That is the digestion path, and it is the highest-probability outcome on a Tuesday following a record close with rising VIX and an elevated oil tape.

The cracks widen. JOLTS prints hot, yields press through 4.55%, oil reverses and extends back above $92, and the tape finally takes the Iran threat seriously. SPY loses $755 and works toward $752. QQQ loses $738 and the air pocket toward $735 opens. That is the fade path. It is not the base case, but it is the first time in weeks the fade path has had this much wind behind it.

The level work below is built for all three.

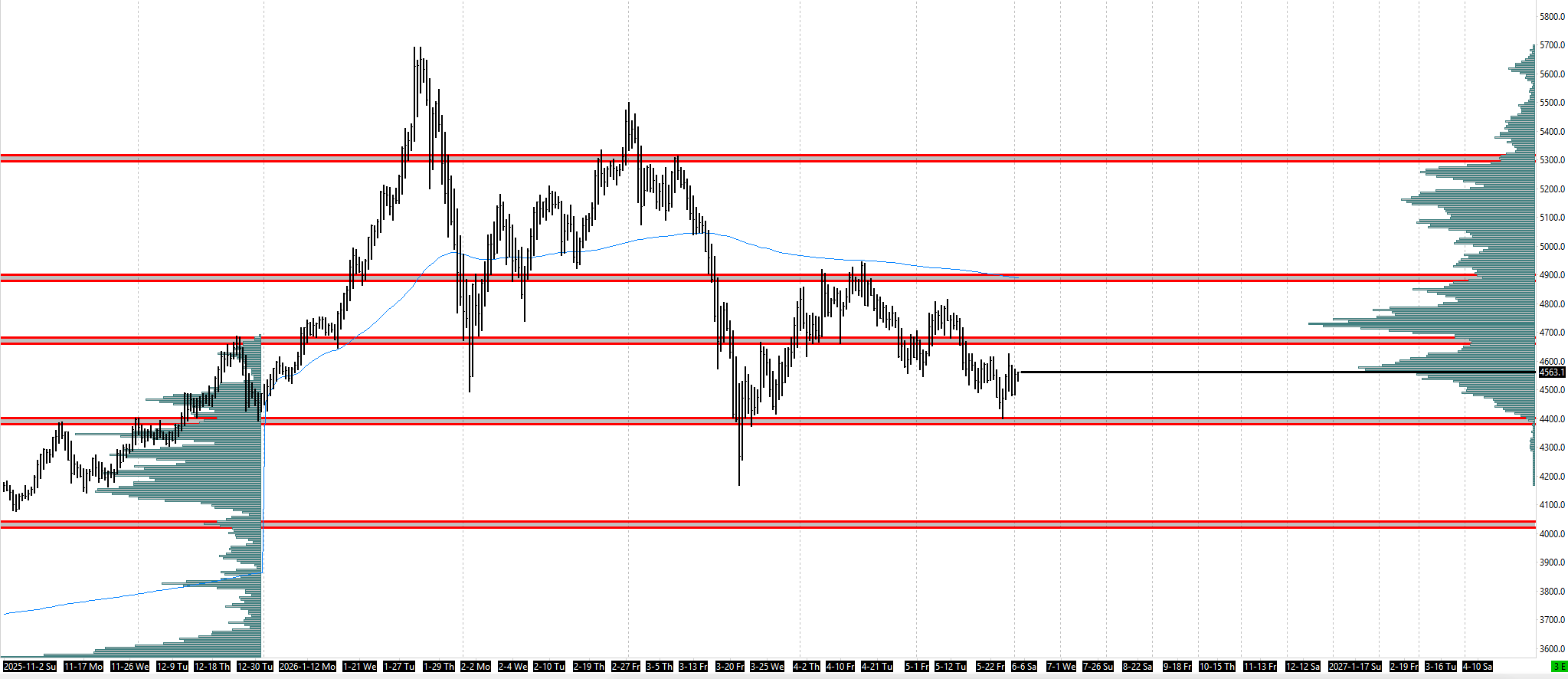

Higher Timeframe Structure — SPY

SPY’s HTF structure remains in clean price discovery after Monday’s $760.28 print. The run from $675 in early April to current is now a 12.5% extension that has held every retest. The breakout shelf at $752 to $755 is the new structural support, with $749 as the prior ATH-turned-floor and the deeper $745 acceptance shelf below.

The HTF read: above $760.28 there is no overhead reference at all. Measured-move math points to $762 first, then $765 to $768 as the deeper extension. Below, the structure is layered: $755 first, then $752, then $749. SPY has every right to extend, but the warning signs that arrived underneath yesterday’s print are the ones that matter most when the index is in discovery. There is nothing to lean on above. There is a lot of structure to fall through below.

Higher Timeframe Structure — QQQ

QQQ’s HTF structure is the cleaner technical story. The Monday $745.65 print extended the post-April run to nearly 17%, with the NVDA news doing the bulk of the heavy lifting in the final session. The breakout shelf at $735 to $737 is the new structural floor, with the deeper $730 to $733 zone as the major composite support. Below that, the $720 to $722 zone marks the prior ATH from two weeks ago.

The HTF read: above $745.65, measured-move math puts $747.50 first, then $750 as the round-number psychological target, then $753 as the deeper extension. QQQ has the highest beta to the AI trade and the highest beta to falling yields, which means it also has the highest downside beta if either narrative cracks. The risk profile has changed even though the price has not.

Higher Timeframe Structure — Gold

Gold’s HTF structure shows the metal sitting at $4,563 in a tight compression after the V-reversal off the $4,400 lows. The $4,500 to $4,600 range has now defined the metal for three sessions. With Iran reescalating overnight, the safe-haven bid should reactivate. The challenge is that rising yields cap the upside even when geopolitics support it.

The HTF read: above $4,563, the $4,600 resistance is the immediate test, with $4,640 the major structural reclaim level overhead. The deeper composite at $4,680 to $4,720 remains the upper reference. Below, $4,500 is first support, then $4,400 as the retest of the recent low, then the $4,360 deeper composite. The metal is decoupling from equities the right way if the Iran story develops. But real yields at these levels keep a ceiling on the move.

🔒 The intermediate structure, intraday execution levels, and three scenario maps for SPY, QQQ, and Gold are below for paid subscribers.

SPY $757.09 premarket below the new $760.28 ATH. QQQ $741.85 below the $745.65 record. Gold $4,563 in compression. Iran reescalating, WTI $91.17 cooling after Monday’s spike, 10-year near 4.50%, VIX 16.14. JOLTS at 10 AM EST. The map below has every level, every scenario trigger, and the playbook for the continuation, the digestion, and the fade.