Broadcom Beats and Drops 12%, Tech Gaps Down, Oil Collapses. NFP Tomorrow. Thursday's Map.

AVGO held its $100B AI target. The tape said that's not enough. Asian semis crater, QQQ down 1.3% premarket, oil cools 4%. Gold bounces.

Roy’s Market Insights | SPY, QQQ and GOLD Premarket Roadmap | Thursday, June 4, 2026

The cracks we mapped Tuesday widened into something real overnight.

Broadcom reported after the close. The numbers were strong by any historical measure. Q2 revenue $22.19 billion, EPS $2.44 versus $2.39 expected, AI semiconductor revenue $10.8 billion up 143% year-over-year, Q3 guidance $29.4 billion against a $28.61 billion consensus. The catch: management held its fiscal 2027 AI revenue target at $100 billion. No upward revision. No raise. The tape did the rest. AVGO opened the after-hours session and dropped 12 to 14%. Asian markets cratered. The MSCI Asia Pacific Index fell 1.6% and halted a four-day winning streak. KOSPI dropped 1.8%, Samsung and SK Hynix lost 2 to 4%, LG Electronics fell nearly 14%. Hon Hai and Wistron in Taiwan dropped 4 and 8% respectively. The AI infrastructure trade just received its first real challenge from inside the camp.

QQQ premarket sits at $734.78, down 1.27% from yesterday’s $744.21 close. That is the first meaningful overnight gap of the entire ten-week rally. SPY is holding up better, $751.59 in premarket, down 0.35% from $754.24. The divergence between SPY and QQQ this morning is the story underneath the story. Mega-cap tech, the engine that has powered every record close since April, is now the source of the weakness.

Yesterday’s session already started the digestion. SPY closed $754.24 down 0.70%. QQQ closed $744.21 down 0.26%. The selloff was driven by an ISM Services PMI that beat at 54.5 versus 53.8 expected, with the Prices Index reaching 71.3, the highest reading since August 2022. ADP was a modest beat at 122K against 117K to 120K consensus. The combination told the bond market that the disinflation thesis is in trouble and the labor market is not loosening enough to give the Fed cover to ease.

The Fed’s Beige Book at 2:00 PM yesterday added to the picture: economic activity little changed across most districts, prices rising at a modest to moderate pace, with tariff-related cost pressures noted broadly. None of that is dovish.

Then the macro tape did something interesting overnight. Oil collapsed. WTI is now $92.32, down 3.85% on the session. Brent $94.34, down 3.55%. The Iran story is fluid, but the oil tape is acting like the worst case is off the table. That is the one piece of news the market wants to celebrate, because falling oil keeps the disinflation thesis alive even with services prices stuck near multi-year highs. Gold bounced from yesterday’s $4,492 low back to $4,525, a partial reversal of the breakdown.

The setup today: tech gap down on Broadcom, oil cooling hard, gold stabilizing, ISM Services confirming inflation persistence, and Initial Jobless Claims at 8:30 AM as the last labor read before tomorrow’s NFP. The 10-year yield is sitting near 4.45% as of premarket. VIX 16.56, up from yesterday’s 16.04. The bid that absorbed every macro shock for ten weeks is now negotiating with itself.

The Institutional Snapshot

SPY · QQQ · Gold | Thursday, June 4, 2026

SPY Wednesday close: $754.24 (-$5.33, -0.70%), intraday range $753.57 to $758.80

SPY premarket: $751.59 (-$2.65, -0.35%), testing the broader breakout zone

QQQ Wednesday close: $744.21 (-$1.95, -0.26%), intraday range $741.01 to $748.65 (new 52-week high at $748.65 then rejected)

QQQ premarket: $734.78 (-$9.43, -1.27%), big overnight gap down on AVGO

Gold futures: $4,525, bouncing from yesterday’s $4,492 low

WTI crude: $92.32 (-3.85% this morning), back below $93

Brent: $94.34 (-3.55% this morning)

10-year yield: ~4.45%, off the recent highs

VIX: 16.56, up from 16.04 yesterday

AVGO premarket: down 12 to 14% after holding fiscal 2027 AI revenue target at $100B unchanged

Asian markets cratered overnight: MSCI Asia Pacific -1.6% (halting 4-day win streak), KOSPI -1.8%, Samsung and SK Hynix -2 to 4%, LG Electronics nearly -14%, Hon Hai -4%, Wistron -8%

ISM Services PMI May: 54.5 vs 53.8 expected (BEAT); Prices Index 71.3 (highest since August 2022); Employment 47.9 (third consecutive month of contraction)

ADP May: 122K vs 117 to 120K consensus

Fed Beige Book: economic activity little changed; tariff-related cost pressures noted across districts

7:30 AM EST: Challenger Job Cuts (May) — prior 83.387K

8:30 AM EST: Initial Jobless Claims — forecast 211K, prior 215K

8:30 AM EST: Continuing Claims

8:30 AM EST: Productivity & Unit Labor Costs (Q1 revised)

8:30 AM EST: Fed Speaker Barkin

Additional Fed speakers throughout the day

NFP tomorrow (Friday June 5) — consensus 85K to 100K, prior 115K

The Setup: The AI Trade Finally Gets Its Test

Ten weeks of records. Three days of warning signs. One earnings report that finally connected the dots.

Broadcom did not miss. AVGO printed a clean beat on revenue, EPS, AI revenue (up 143% year-over-year), and Q3 guidance. The stock fell 12 to 14% in extended trading because the long-term AI target stayed flat. That is the kind of reaction that tells you positioning is the problem. When good news is not good enough, the trade is crowded. When the trade is crowded, the unwind happens fast.

Two things make this different from Monday’s warning signs.

The Asian tech selloff overnight is the contagion test. When Samsung, SK Hynix, Hon Hai, Wistron all sell off together on a Broadcom guidance disappointment, the market is telling you the AI capex narrative is being repriced globally, not just at one US name. That is the kind of cross-asset signal that does not show up in a chart until you see how the US session opens.

The oil collapse is the offsetting macro tell. WTI down 3.85% is doing real work to keep the inflation thesis intact. If oil keeps cooling through the day, the bond market gets reasons to relax. That gives equities room to absorb the Broadcom shock without a full-fledged risk-off session. If oil reverses higher, the picture changes fast.

Three scenarios stay in play for Thursday.

The tape absorbs Broadcom the way it absorbed everything else for ten weeks. AVGO finds a floor in the 12% drop range. SPY holds $750. QQQ bases at $735 and reclaims $740 by mid-session. Jobless Claims comes in line. The bid returns into the close as positioning shorts get squeezed. That is the resilience path. It is harder today than at any point in the rally.

The tape digests. AVGO settles at down 10 to 12%. SPY balances $750 to $754. QQQ rotates $735 to $740. Jobless Claims and Fed speakers create noise without direction. The session ends mixed, setting up Friday’s NFP as the decision point. That is the highest-probability outcome.

The tape extends the crack. AVGO stays at down 12 to 14% and drags the rest of semis with it. SPY loses $750 and the $748 to $745 zone activates. QQQ loses $735 and the air pocket toward $730 opens, then potentially $725 if mega-cap tech finds no buyers. That is the fade path. It is the cleanest setup for a real flush in a month.

Higher Timeframe Structure — SPY

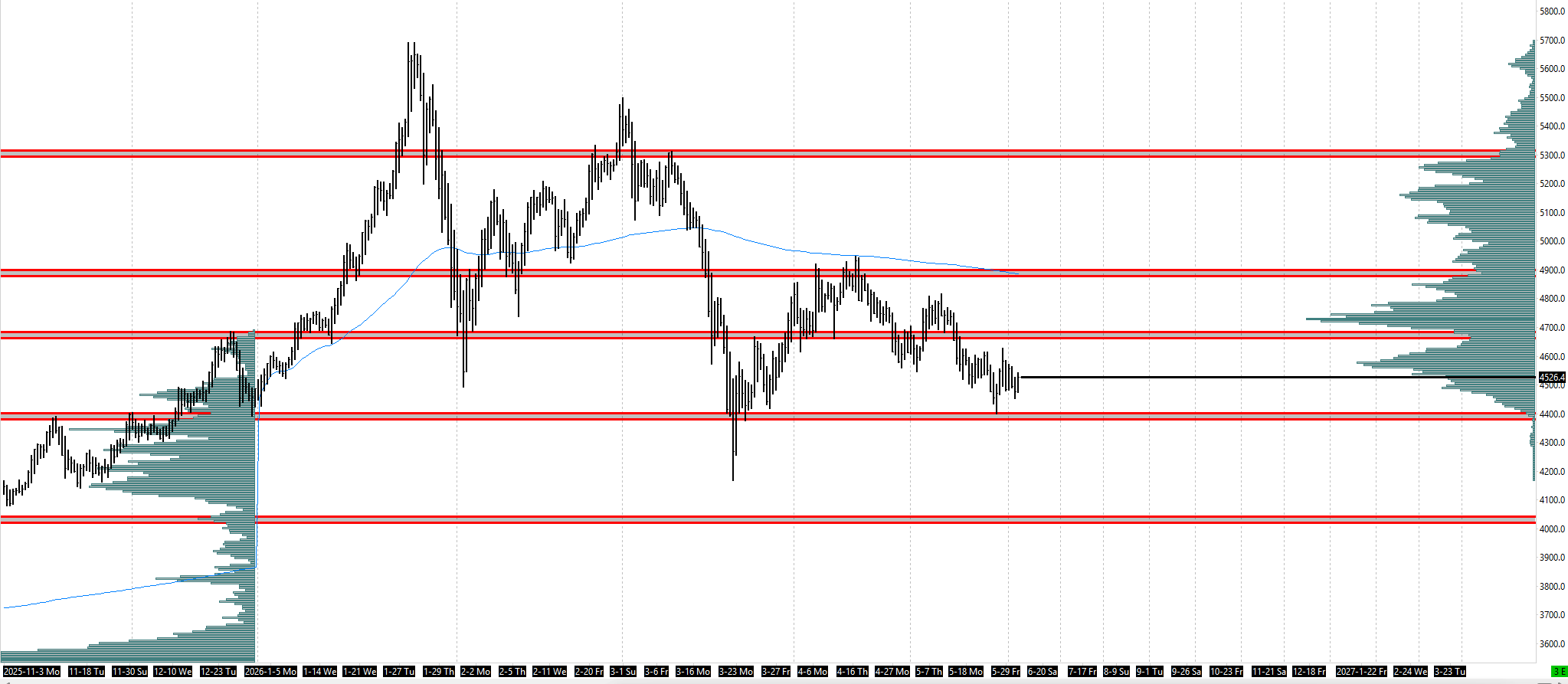

SPY’s HTF structure has cracked the immediate breakout shelf but remains inside the broader post-April uptrend. Yesterday’s close at $754.24 lost the $755 to $757 zone and put $750 as the round-number floor in play. The $748 prior compression sits just below, with $745 as the broader acceptance shelf and $740 as the deeper composite. The post-April uptrend itself remains intact until the index loses $745 with acceptance.

The HTF read: above $755, the $758 zone is the first reclaim, with the $760.40 ATH as the major test. Below, $750 is the round-number magnet, then $748 (prior compression), then $745 (broader acceptance), then $740 (composite). The structure is layered and deep, which means SPY can digest hard without breaking the uptrend. The level that decides whether this is a digestion or a breakdown is $745.

Higher Timeframe Structure — QQQ

QQQ’s HTF structure took the bigger hit. Yesterday’s close at $744.21 held the breakout shelf at $740. The premarket gap to $734.78 puts the index back inside the prior $735 to $745 range, undoing the entire breakout from May 30 to June 2. The $730 to $733 zone is now the deeper composite, with $727 as the structural pivot and the $720 to $722 prior ATH zone as the major reclaim level on a real flush.

The HTF read: above $735, reclaim attempts target $740 first, then $744 (yesterday’s close), then $746 to $748 as the breakout retest. Below, $733 is the deeper composite, then $730, then $727. QQQ has the highest beta to the AI trade and the highest beta to falling yields. Today’s session tests both: AI is being repriced via AVGO, and yields are easing on the oil collapse. The path of least resistance depends on which beta wins the morning.

Higher Timeframe Structure — Gold

Gold’s HTF structure showed a tradeable bounce off yesterday’s $4,492 low back to $4,525 this morning. The $4,500 round number is back to acting as support rather than resistance, which is the first constructive signal in three sessions. Above $4,525, the $4,560 upper-edge resistance comes back into play, with the lost $4,640 structural floor as the major reclaim target. Below, $4,500 is now the line that decides whether the bounce holds or the $4,400 retest reactivates.

The HTF read: above $4,525, the bounce extends toward $4,560 if oil keeps cooling and yields keep easing. Above $4,560, the lost $4,640 floor becomes the major test. Below $4,500, the breakdown reasserts with $4,480 LVN first, then $4,400 retest. Gold is back to acting as the cleanest macro proxy on the board. Falling oil, falling yields, and rising risk aversion in equities all support a bid.

🔒 The intermediate structure, intraday execution levels, and three scenario maps for SPY, QQQ, and Gold are below for paid subscribers.

SPY $751.59 premarket testing the broader breakout zone. QQQ $734.78 premarket down 1.27% on the Broadcom gap. Gold $4,525 bouncing from $4,492. WTI $92.32 down 3.85%. AVGO down 12 to 14% extended hours. Initial Jobless Claims at 8:30, Challenger 7:30, Fed Barkin 8:30, more Fed speakers all day. NFP tomorrow. The map below has every level, every scenario trigger, and the playbook for the resilience, the digestion, and the fade.